Cryptocurrency: What It Is and How It Works

Cryptocurrencies are digital or virtual currencies, secured by cryptography. Most of them are based on decentralized blockchain networks, enforced by a network of separate computers and don’t have a formal centralized server. Most of these networks are voluntary, global and based on the use of its open-source software.

A defining feature of cryptocurrencies is a lack of any central authority, which allows for their theoretical immunity to government interference or manipulation.

Cryptography and presence of a distributed ledger in a form of blockchain exclude the possibilities of forgery and double-spending in cryptocurrencies.

The emergence of cryptocurrencies has a vast historical and political context surrounding it – decentralized digital currencies took a position of stark contrast with traditional fiat money when dissatisfaction of state-run centralized currencies reached a threshold in the society during the Great Financial Crisis of 2007–8. And since their inception, cryptocurrencies have already had an enormous worldwide economic influence. Cryptocurrencies are still a maturing economic medium and their full potential is surely yet to be realized in the future.

But for us to understand the premise of the cryptocurrency, it’s important to pinpoint its role and its implications in the larger economic role and philosophy, beginning from the ground up.

First of all, since cryptocurrencies are decentralized and in most cases meant for exchanging between users directly, they all function as a decentralized P2P (peer-to-peer) payment system. Let’s start from the ground up and build our way towards the cryptocurrencies.

So, what’s a decentralized payment system?

You’ve probably been familiar with decentralized payment systems or exchanges in one form or another ever since your childhood, offline.

The prime example of a native P2P payment system is exchanging various items with our friends and acquaintances in school: like pokemon cards, stickers or other little valuables, which were important to our social group in those times. There’s usually a system installed, where the value of those items and their equivalent is agreed upon between all participating parties – your friend group (e.x. 1 sticker = 3 pieces of candy, 3 stickers = 1 card , etc.). In order to “log into” this system, you would still have to spend real assets (or your parents assets). There’s no authority dictating the value of these items, it’s formulated by the demand. So, if a certain group of people is interested in such an exchange, the system starts working. The result is a P2P network where everyone is equal and no one has special privileges. It’s a basic economic interaction on a decentralized basis.

Now, Let’s try to put this in digital and make our way to crypto. But we’ve still got a long way to go.

Digital P2P

The prime forms of digital P2P interaction (of course, we are talking about the time before the introduction of Bitcoin, the first cryptocurrency), were file sharing systems, which originated in the 2000s, like Napster, Limewire, Freenet or BitTorrent.

The basic idea was very simple: individuals made files available for download from their own machine. Other users could see what the users in the system made available, search for files they desire and download them from a peer who has made it available for downloading.

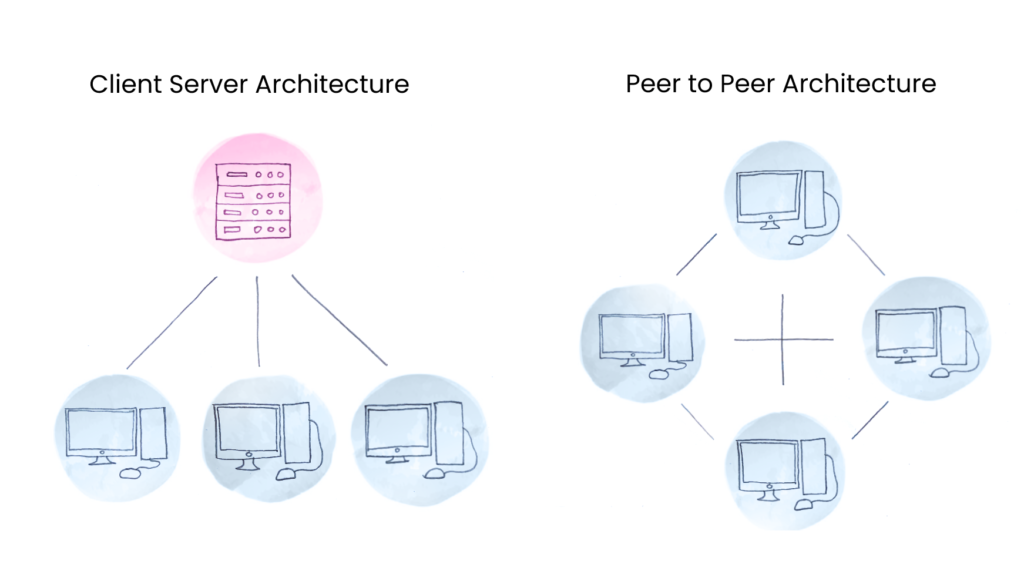

In contrast to client-server networks where all network content is located in a central location, P2P resources are located in and provided by computers at the edge of the network (a.k.a. “peers”), hence no central authority to rely on. This is what allowed for such a wide variety of content to be distributed through these networks, a lot of copyrighted media too, which eventually got them in trouble with the law.

Those systems had a working, but fairly unstable incentivization mechanism, a shaky scaling potential, problems with free-riding and lack of motivation for keeping the downloaded file available (seeding). Much of the design of these P2P programmes relied heavily on altruism and ethics of its users, which is a nobel, but a naive concept, not suitable for a basis of an economic model (nor it tried to be such).

These systems were really products of their era, technical no-hows, which, however, introduced the P2P type of communication to the internet on a big scale. And in a way this made its contribution to the subsequent rise of cryptocurrencies.

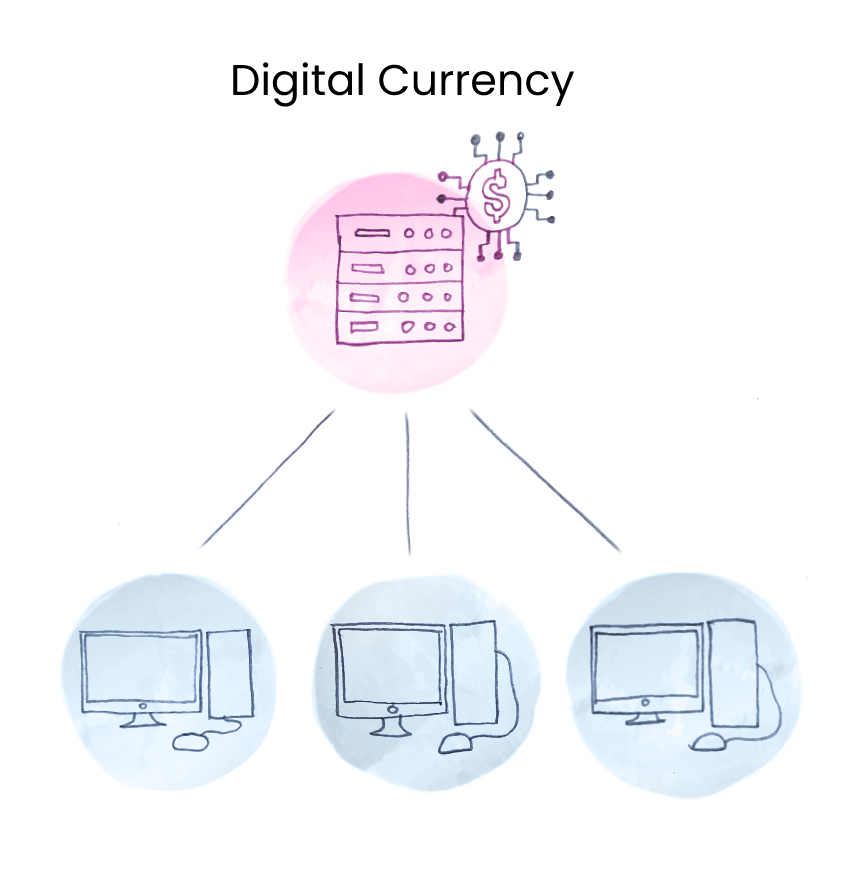

Digital currency

Meanwhile, the turn of the millennium and its advances in information technology also provided context for an unprecedented emergence (and eventual sinking) of various digital currencies (not yet talking about cryptocurrencies), such as e-gold, e-Bullion, Liberty Reserve, Pecunix, and many others, their main attractive being allowing for instantaneous transactions and borderless transfer-of ownership. This concept also included “fictional” virtual currencies only used in the

context of particular virtual communities, such as World of Warcraft’s in-game gold and Second Life’s Linden Dollars, or frequent-flyer and credit card’s loyalty programs

points.

But the digital exchange still had a bunch of setbacks that had to be solved before the exchange could become truly fair and uninterrupted. Those setbacks were in the existence of the centralization – the middleman, an entity which has the power to regulate, and the lack of transparency, which implies heavy emphasis on trust. Middleman knows private info and can fake and use assets by himself

Middleman can counterfeit deals (his friends sell the same asset to multiple people and the middleman approves it). Middleman can change the rules of the interaction, which introduces significant risks for the stability of the whole system.

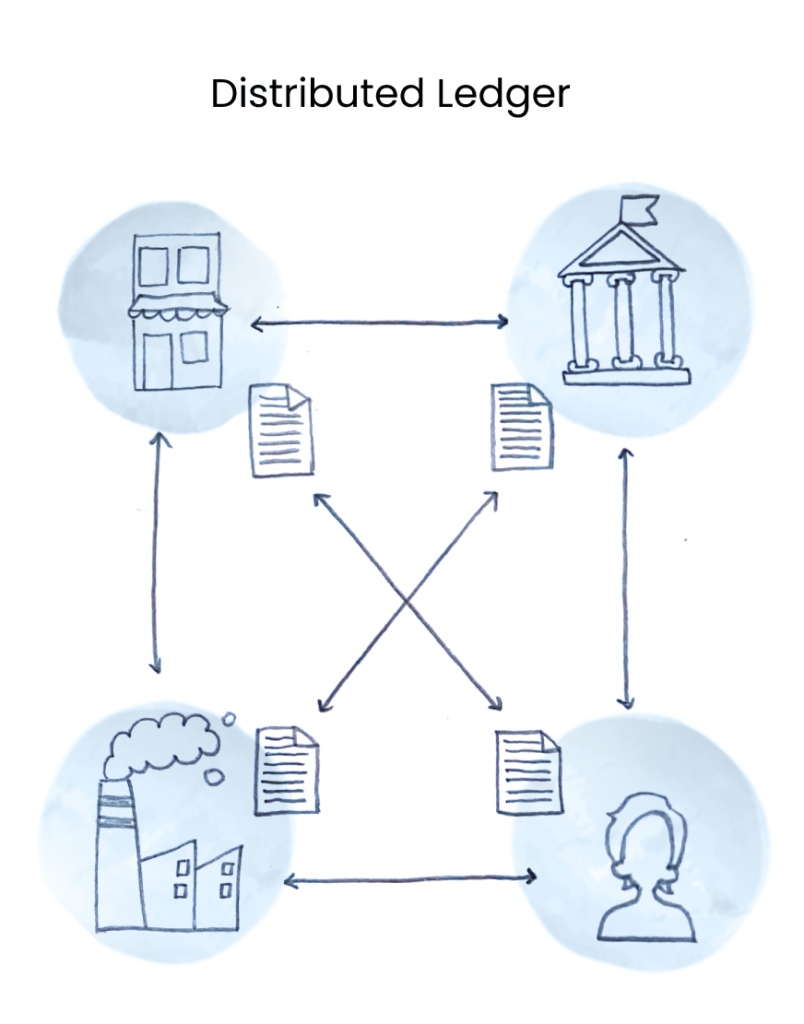

Digital P2P + Digital currency. Blockchain

If we summarize all of the setbacks of digital currencies were basically just the symptoms of a centralized system. So why not try realizing the digital currency in P2P. This way we get rid of the centralized servers, and replace the middleman with the system, where every community member is in fact a middleman for every other community member. This is very easy if everybody has a hold of every action of every asset in the community. Something like a universal ledger, available to all, and kept by all. This ledger is what is called a blockchain.

Now every actor in the system keeps track of the actions of all the actions in it. Everybody keeps the same copy of the receipt instead of the central authority.

A receives 5 assets.

B receives 10 assets.

A sends 5 assets to B.

B sends 15 assets to X.

At any moment of time every member of the community knows all the dispositions of each asset in the system. There is no need to “take a look”, “ask”, or “check”. In other words there is no need to trust anybody, because the member already has all the information on the blockchain.

Blockchain is a digital way to create a transparent environment in P2P systems. The main objectives of blockchain are:

- To combine all information (all transactions in the system) in blocks

- Link one block to another without possibility to replace it in future with cryptography methods.

- Provide a convenient way to add transactions into these blocks.

How blockchain works:

The way the blockchain works, that it has groups of transaction (roughly as in our previous example) records represented within a block – a unit of information, whose valid connection to the remaining blockchain must be verified and approved.

Here’s what a block looks like in Bitcoin.

Copies of the proposed transactions are broadcast to a vast, decentralized peer-to-peer mesh network of nodes with “flat” topology architecture on top of the Internet,

running the Bitcoin client software that takes the job of validating the transactions

But you should remember that while blockchain is a byproduct of development of the first cryptocurrency – Bitcoin – it can be used outside of the cryptocurrency system and utilized for banking, gaming, loyalty programs, digital signatures, etc.

Cryptocurrency as a core of digital p2p systems.

So, the blockchain fixes interactions and trust problems with transactions, but there are still issues with third-party assets themselves (like digital currencies, gift-cards or loyalty points). Users may use blockchain as a recording of transactions of those third-party assets, but because of their third-party nature, there is a threat that the assets will be doublespent or counterfeit (although it will not affect the blockchain recordings). Also, if the assets we are talking about are centralized-issued, they can have mandatory restrictions too, preventing complete freedom of their trade.

So now we’re finally getting to the cryptocurrency part. And what Bitcoin has introduced to the world is that the most crucial part of the markets – money themselves – can be brought to the P2P. It created a “peer-to-peer electronic cash system” with its own intrinsic asset.

Emitting our own assets helps to create a trust zone inside this environment (because rules behind these assets are transparent and open). If there is cryptocurrency, there is no way to bring other assets from outside of the system, thus no way to affect the monetary policy doing it outside of blockchain.

This environment can be pictured as an enclosed glass box with a lot of hand-size holes and balls inside: you can hold them, touch them, trade them, but you can’t put it out or put a new one inside. These balls can’t be doubled. It is easy to join the system and get yourself some of them. And there is no middleman in this absolutely trustless environment.

In this way cryptocurrency follows these three important principles:

- It is owned and controlled solely by the holder. Nobody can take your crypto-holdings within a system and there is no middleman to burn or double it.

- Also, this system is permissionless: everybody can connect and participate in trading, obliging the rules.

- A value of cryptocurrency also emits from its security, discreteness and a direct connection to a user.

As for the crypto part, cryptocurrency received its name because it uses encryption to verify transactions. This means advanced coding is involved in storing and transmitting cryptocurrency data between wallets and to public ledgers. The aim of encryption is to provide security and safety.

BTW, It’s interesting that the idea for cryptocurrency first emerged far before the emergence of Bitcoin, in 1983, when American cryptographer David Chaum published a conference paper outlining an early form of anonymous cryptographic electronic money. The concept was for a currency that could be sent untraceably and in a manner that did not require centralized entities (i.e. banks). In 1995, Chaum built on his early ideas and developed a proto-cryptocurrency called Digicash. It required user software to withdraw funds from a bank and required specific encrypted keys before said funds could be sent to a recipient.

Upkeepers of the Ledger. How cryptocurrency is used for incentivization within its system

So, the ledger we were talking about – the blockchain – it contains not just a couple of lines of transactions, it’s a lengthy ledger with every transaction in the system that is being constantly synchronized by all of the actors in the system.

Imagine this blockchain growing to 1 million accounts. It means that every transaction on the blockchain should create 1 million copies in one million accounts. And it should be done by every user, even those, who don’t make transactions, if they want to participate in the system. Try to imagine 5 thousand of such operations – that’s 5 billion records! And what if these operation logs are quite hefty? The whole process might slow down almost to a halt.

How does cryptocurrency solve this issue? It delegates the task of verifying transactions and keeping the full ledger to Nodes/Miners – volunteers who take this job for a profit within a system. Miners/Nodes provide their computing power to run blockchain software and keep the record of the whole blockchain while being in constant communication with other nodes in this blockchain, checking it out for potential fraud and double spending. The more nodes there are in the system, the more secure and stable this system is. For example, Bitcoin currently has over 14 thousand nodes, which ensure the stability and fairness of exchange. And as we will see further, these nodes operate for profit. They get rewards in the form of cryptocurrency for their work.

And this is actually the process of emitting/creating most of the existing cryptocurrency. For example, Bitcoin is generated using Bitcoin mining. But, with that said, not every cryptocurrency uses mining to generate new coins, and coins can be created in some other ways.

How exactly coins are created depends on what is defined by a given cryptocurrency’s code. For example, instead of mining or mining alone, a cryptocurrency may create some tokens upon launch as developer rewards, or a cryptocurrency may reward tokens as interest to holders of a token. The code of the cryptocurrency defines things like maximum supply, mining rewards, etc.

Proof of Work and Proof of Stake

Core of crypto is its consensus mechanism – the method of verification of transactions.

A lot of transactions are verified through a Consensus mechanism called Proof of work. This is a consensus, where participants agree that those who put in the computing work, creating new blocks, and whoever manages to do it faster, are rewarded with a cryptocurrency of the blockchain. Thus, the creator of new blocks proves his interest in the stability of the system. This type consensus usually means fiat investments, particularly, investment into the hardware, that would allow for faster mining. POW blockchains usually have the fastest nodes.

Proof of stake was developed to reduce the amount of power needed to verify transactions. This is a consensus, where participants agree, that proving your interest in the stability of the system is based on you freezing and holding a share of the assets, giving up your opportunity to sell them. This works as proof, that the further expansion of the network is more important to the holder as momentary gain. And these holders would get a reward for each validated transaction. And any attempt at manipulating the ledger and scamming the system results in nodes losing their investments.

Consensus keeps the nodes in agreement with each other and users and keeps the nodes interested not only in stability, but in further development of the network (so that their assets would expand too), and keep the whole network offloaded and transactions – fast and easy.

In other words, the nodes have a lot to lose in case of a system failure and a lot to gain in case of its prosperity.

Supply:

Cryptocurrencies vary greatly in supply in terms of its volume and type. The supply of a particular cryptocurrency refers to the total number of coins in circulation. Three essential terms relate to supply:

Fixed (or maximum) supply – the total number of coins that can ever be in circulation.

- Circulating supply – the total number of coins in circulation. It defines how many units of that cryptocurrency are swirling around the market at any one time. As of this writing, there are over 19 million BTC, 122 million ethereum (ETH) and 67 billion tether (USDT) coins in circulation, for example.

- Total Supply – total number of tokens that exist on the blockchain, including tokens that aren’t in public circulation. When a cryptocurrency project launches a new token or coin, they might create lots more crypto than they distribute at that moment. For instance, coins earmarked for staking rewards – those given to people who lock up tokens within a protocol – might technically “exist” on the blockchain, but you might not be able to start earning them until a certain condition has been met or date has been passed.

- The maximum supply of Bitcoin for example is limited to 21 million. In other words, it is deflationary by nature. As a result, not more than 21 million Bitcoins can ever be mined or be in circulation at any given moment.

There are currently over 19 million bitcoins in existence. This number changes about every 10 minutes when new blocks are mined. Currently, each new block adds 6.25 bitcoins into circulation. Based on the current schedule, all Bitcoin will be mined and in circulation by the year 2140, which leaves a significant amount of time ahead for the network to grow and become more globalized.

Other tokens, like Ethereum, have a constant flow of new assets added to the ecosystem, which makes them inflationary. Most cryptocurrencies follow a demand and supply principle that determines their growth.

Share

Receive updates from our blog

You may be interested

Learn basics in our free Wiki section!